Getting money in the bank after fundraising does flavor like sweet victory for startups. But the engagement is only half earned. The need to optimally succeed money is among the firstly action items that the founders need to address.

“Fundraising is an extreme sport,” said Marc Pitman in his work,” Ask Without Fear “. While he was referring to philanthropy, the saying is equally true for fundraising by startups.

After a series of small-time excruciating outings embedded into the larger fundraising process, coming that fund in the bank does experience like sweet succes for startups. But the clash is only half earned. The fundraising can be compared to procuring ammunition for a long-drawn battle- indispensable, but not the exact purpose of your startup.

The need to optimally organize money is among the firstly action items that the founders need to address. And the tour of money management begins with one basic questions 😛 TAGEND” Is there a smarter alternative to a Current Account ?” Perhaps a bank fixed sediment? But interest rates have precipitated so much better. Or will a mutual fund be more efficient? But then what about the “subject to market risk”? But I’ve heard even gigantic companies invest in mutual funds, right? Is all of these meant for bigger companies merely? Am I better off with the relied chequing account and deposited lodge?

Founders often grapple with all these questions. They get advice from various parts like their bankers and brokers.

Let’s talk about the first leg of money management for startups: Devoting freshly raised funds.

Here are a few preliminary factors that you may need to consider before deciding on the right investment avenues.

Visibility on shine: You would have worked on a cash flow projection for your fundraising pitch. It might require some adjustments to reflect the changes in the overall business mean if any.( e.g. change in capital invoked, more aggressive competition, need for branding wastes etc ). The objective is to have a closer-to-reality view of expected cash flow. Your cash flow projection needs to answer,” How much money will I need every month for the next n number of months ?” where “n” is the period you expect the conjured fund to last.Check on duty applicability: Most venture-funded startups are loss-making and hence there is no tax relevant. Nonetheless, it helps to be sure about the pertinent tax rate under the” Income from Business” is chairman of the Income Tax rules.Check legal status: Take a note of your Shareholder Agreement to check for clauses around controls and predilections in respect of the avenues for non-core or non-operating fund deployment.

Once there is clarity on the above needles, we must move to define the objectives and guidelines of the treasury investment. Drawing upon our experience in managing treasury for several startups, here are the most common guidelines 😛 TAGENDLiquidity: Changeable is an understatement when it comes to describing a startup’s pilgrimage. While parking surplus funds, do not lose focus on liquidity, as it is of paramount importance to startups.Risk-minimisation: No asset is 100 percent risk-free and don’t let anyone tell you otherwise! Investing is about understanding the health risks involved, being cognizant of the appraise at risk, become aware of possible mitigation techniques, and then making an informed decision. The notion is to minimise perceptible danger. No investor would ever want to see you use the money conveyed for your core business being utilised to generate capital gains.Return-optimisation: Return on Investment should be in line with the degree of risk involved in the investment. The risk-reward trade-off should make sense, always.

Now that we have clarity on the essential points to make a sound investment decision, tell us dive into the details of the investment process.

Investment overseers approach treasury investing in different ways, including looking at choice of instruments, programme edification, and the extent of active administration. However, we will focus on a rather simple yet highly effective strategy that startup founders who come from non-finance backgrounds can follow.

We call this the slice-and-match method.

The approach focuses on slicing the period for which you expect the grown amount to last into smaller seasons( monthly or quarterly) and then match the most suitable products/ instruments for each slice- obstructing the guidelines and objectives constant throughout.

Here is an example of the slice-and-match method.

* For immediate utilisation( 0 to 1 month)

For the amount you require immediately( over the next month ), there is no recommended alternative to your good aged current account.

For those trying to squeeze every bit of optimisation, Overnight monies could be your best bet. Overnight Mutual Funds invest in overnight defences having a maturity of one day. This segment has negligible danger show, generally no exit onu and will generate more than the 0 percent that you get on a current account.

The only thing you must be cognizant about is, the conventional recovery processing date before the amount gets ascribed into your current account. Annualised furnishes within the limits of~ 2.75 percent-3 percent is expected to continue, based on current returns.

Contingency Reserve

Carve out anywhere between 15 percent-2 0 percent of the residual fundraise and invest it straight away into liquid monies, before moving to the next slice.

* For very near-term utilisation( 1 month to 6 months)

This is where we begin optimising returns on investment. For the money that you require over the next one-six months, liquid stores serve as a great avenue.

Liquid stores invest in fixed income and money market insurances with a maturity of up to 91 days. Given the very short-term maturity and often high-pitched recognition quality of instruments the category invests in, gamble show is extremely low. As on the year of writing this note, it would be safe to assert that no investment in a liquid money has ever resulted in a negative return, if held for over a few months. Annualised returns can be expected to be in the range of 3 percent-3. 5 percent for some time now.

* For near-term utilisation( 6 months to 12 months)

For the amount required for utilisation in the next 6 to 12 months, an investment can be made into a combination of ultra-short duration monies and low-pitched duration funds.

Ultra-short and low-grade period stores invest in fixed-income defences maturing in approximately 3-6 months and 6-12 months, respectively. Duration risk( likelihood due to change in interest rate; also see note below) is the potential at this moment. But it can be mitigated if the amount devoted is held for appropriate spans. An proper period would be to stay invested in the ultrashort funds with the amounts required in months 6 to 10 and in low-grade span funds for the amount required for month 11 and 12.

Expect returns for ultrashort and low-spirited duration funds to be in the range of 3.5 percent-4 percent for some time now. The store is subject to minimum periodic volatility due to duration risk.

What is duration risk?

Duration risk is also known as interest rate hazard. Now is a rather simplified explanation — Fixed income or indebtednes certificates’ premiums are inversely proportional to the interest rate movement. When key interest rates like that of mark government insurances or RBI’s repo addition, the price of other fixed-income insurances precipitate ensuing in a temporary loss, known as ” mark-to-market ” loss and vice versa.

The duration risk mounts as the maturity of the debt instrument multiplies. The peril can be mitigated if the asset is held till maturity or in case of mutual funds, closer to aggregate effective maturity of the fund.

* For short-term utilisation( 1 year- 2 years)

This bucket is the sweet spot for bank defined deposits. Given the current interest rate scenario, banks are willing to offer the best they can for situates willing to be committed for a period of 1 to 2 years. Typical rates offered by the large public sector or private planned commercial banks should be in the range of an annualised 4 percent-4. 5 percent.

You can consider investing in FDs of smaller banks like small-time commerce banks which give a higher interest rate, but they come with greater likelihood as they might not be able to weather a rough fiscal cycle.

If you are looking to optimise through relatively higher interest rates offered by small-scale commerce banks, try not going beyond the Rs 5 Lakh as accumulations up to Rs 5lakh are insured by RBI under Deposit Insurance.

An alternative to bank set monies for the same period could be continued investment into a combination of ultra-short, low-duration and the more flexible money market funds. Annualized blended-average return for the three categories could be in the range of 3.7 percent-4. 2 percent. Also, mutual funds volunteer more liquidity, unlike bank defined lodges which are typically non-withdrawable or withdrawable with foreclosure a sentence of around 1 percent.

While we’ve been presuming no tax consequences, there’s merit in understanding the tax laws on debt mutual funds and cooked accumulations and considering post-tax returns before making an investment decision.

What is the taxation on obligation mutual funds?

For speculations held up to 3 years, the increases are taxed as Short-Term Capital Gains at a pace equivalent to the applicable income tax rate. For accommodating interval over 3 years, the additions are levied at 20 percent with indexation. Nonetheless, unlike bank FDs , no TDS is rebated on debt mutual funds.

* For medium to long-term utilisation( 2 years and above)

Bank specified sediments continue to be an optimal choice for this bucket as well. The next best alternative is to explore what debt mutual funds have to offer. Within debt mutual funds, it is imperative that we curb to liquid, ultra-short, low-grade period and fund market strategies; moving into any list beyond it could go against the guidelines we defined at the beginning.

For those willing to hold some quantity beyond three years, Banking and PSU debt funds could be a good category passed exceedingly less vulnerability to credit risk( the health risks that the investor may not receive the principal and the best interest ), but some degree of duration risk. A mixed median of the portfolio with around 25 percentage allocated towards the Banking and PSU Debt Fund should yield an annualized return in the range of 4.2 percent to 5 percentage for some time now.

Do not even worry about optimising this amount any more, as any attempt to over-optimise will push you down the alley where threat will outweigh the benefits.

Founders may be invited to give into fancy cash management schemes, corporate prepared sediments, direct debentures, NCDs and a variety of concoctions sloped by various authorities as high-return alternatives, but we strongly recommend against such investments.

A utterance of caution:

The number of mutual funds available and choice of sterilized lodges could be overwhelming. While the above strategy is pretty much do-it-yourself, it is advisable to avail professional advice from a region expert on the choice of fund and situate to optimise further.

A few things to keep in mind when considering makes other than what has been discussed so far.

Instruments reward you for the degree of risk you are willing to take. If person offers too good a return, be sure to understand the degree of risk involved.Unless you are in the business of investing, the funds you have raised is primarily meant to be deployed in financial assets for fund advantages. There is no reason for you to chase a couple of extra basis points.Whenever in doubt, be conservative.

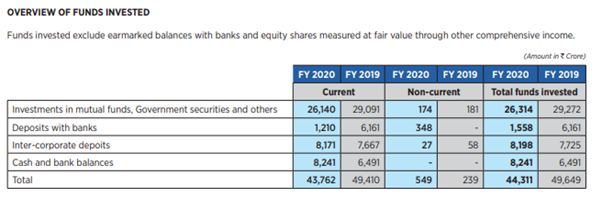

Case-in-point: Investment profile of TCS( Source: TCS Annual Report 2019 -2 0 ):

Major allocation to Mutual Fund and Government Securities

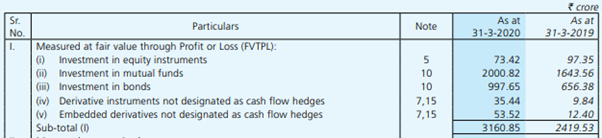

Case-in-point: Category-wise classification for relevant financial assets of L& T( Source: L& T Annual Report 2019 -2 0)

Key allocation to Mutual Funds

😛 TAGEND

Read more: yourstory.com

Recent Comments